Regional Phillips Curve in a Small Open Economy: Evidence from Bolivia

Recently, together with my friend and co-author Hugo Vaca Pereira, we wrote the working paper “Regional Phillips Curve in a Small Open Economy: Evidence from Bolivia”. In this work, we estimate the relationship between inflation and the output gap at the departmental level using quarterly data for the period 1993–2019.

The central result is that the relationship between inflation and economic slack is small and, in most specifications, statistically indistinguishable from zero. This finding holds under estimators that control for common factors, allow for regional heterogeneity, and incorporate inflation dynamics. Even when separating inflation into tradable and non-tradable components, the relationship remains weak.

In simple terms, the evidence suggests that inflation dynamics in Bolivia exhibit a strong common component and limited sensitivity to regional cyclical conditions. This has important implications for understanding the channels through which monetary policy operates, particularly in a context of elevated inflation and institutional constraints such as the one Bolivia currently faces.

In this post, I share some elements of the research process, the main results and their interpretation, as well as my view on the implications these findings have for the current debate on monetary policy in Bolivia.

The Research Context: What Causes Inflation?

For those interested in monetary economics, the question of what causes inflation remains central—and, in some sense, unresolved. Decades of research have not produced a single, unequivocal answer.

One classic explanation holds that inflation is ultimately a monetary phenomenon: if the money supply grows faster than output, prices must adjust upward. This is the intuition behind monetarism—the idea of “too much money chasing too few goods.”1

However, while this relationship may hold in the long run, it is less convincing as an explanation for short-run inflation dynamics. The experience following the Global Financial Crisis of 2008 is illustrative: both in the United States and Europe, monetary aggregates expanded significantly without a proportional response in inflation.

Such episodes reinforced the current operational framework of central banks, which do not directly control the money supply but instead conduct monetary policy through interest rates. In this framework, short-run inflation dynamics are typically modeled through the New Keynesian Phillips Curve (NKPC), which relates inflation to expected inflation and the output gap:

$$ \pi_t = \pi_t^e + \kappa x_t + u_t $$

where $\pi_t$ denotes inflation, $\pi_t^e$ expected inflation, $x_t$ the output gap, and $\kappa$ the sensitivity of inflation to cyclical conditions.

The intuition is straightforward: if inflation expectations are anchored—say, due to central bank credibility—then fluctuations in inflation depend primarily on the output gap. When actual output exceeds its potential level (a positive gap), aggregate demand pressures productive capacity. Firms face higher marginal costs—whether through rising wages, more intensive capital utilization, or bottlenecks—and pass part of these higher costs on to prices.

Under this logic, if the central bank can influence the output gap—for instance, by adjusting interest rates—it can indirectly influence inflation. This is the operational foundation of modern monetary policy.

Project Motivation

The initial intellectual spark for this project emerged during a monetary economics class in the Master’s in Banking and Financial Regulation at the University of Navarra, taught by Vítor Constâncio. That discussion raised a more specific question: how relevant is the Phillips Curve in Bolivia, given its structural and institutional characteristics?

Around the same time, while listening to the podcast Macro Musings by David Beckworth, I came across an interview with Jonathon Hazell about his recent work on the regional Phillips Curve in the United States.2 The identification strategy struck me as both simple and elegant.

If expectations and the monetary regime are common across regions within a given period, then they need not be measured directly. Instead, one can compare regions within each quarter. The slope of the Phillips Curve can be identified using cross-sectional variation—regions with higher or lower output gaps—while time fixed effects capture common shocks and unit fixed effects absorb structural characteristics specific to each department.

Formally:

$$ \pi_{i,t} = \alpha_i + \delta_t + \kappa x_{i,t} + u_{i,t} $$

With the idea clarified, the question became empirical: could this strategy be implemented for Bolivia?

Data

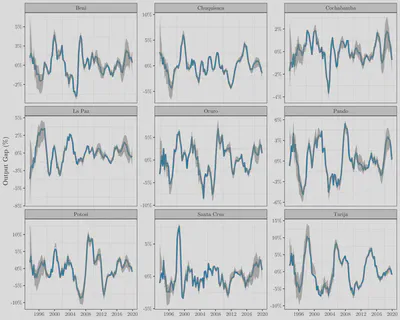

The first serious obstacle was data availability. Bolivia’s National Institute of Statistics (INE) does not publish quarterly GDP by department. Without a regional measure of the business cycle, the strategy would not be feasible.

The project became possible thanks to quarterly regional GDP estimates developed by Miguel Chalup and Fernando Escobar3 during their time at Bolivia’s Ministry of Economy and Public Finance. These series allowed us to construct departmental output gaps and operationalize the panel estimation strategy.

With the data in hand, the question was no longer whether we could estimate the model, but what we would find.

Preliminary Results: An Uncomfortable Finding

The first results were, in a sense, uncomfortable.

The relationship between inflation and the output gap at the departmental level was small and statistically indistinguishable from zero.

If the Phillips Curve is the central transmission mechanism of monetary policy in the short run, how should one interpret a coefficient that is effectively zero?

At this point, Hugo’s academic experience became crucial. What initially appeared to be an interesting result evolved into a more ambitious research project: if the relationship is weak, we must ensure that it is not an econometric artifact.

Methodological Extensions: Is It a Specification Issue?

Once the preliminary result—a small and statistically weak slope—was established, the next step was to rule out that the finding was driven by specification choices or data construction. In the paper, we extend the analysis along three main dimensions: cross-sectional dependence, tradable/non-tradable decomposition, and robustness to output gap measurement.

1. Cross-Sectional Dependence and Common Factors

A key diagnostic was that departmental inflation in Bolivia moves in a highly synchronized manner. Correlations between regional and aggregate inflation are high, and formal cross-sectional dependence tests reject weak independence across units. This suggests that common factors—such as external shocks, the exchange rate regime, or administered prices—may dominate inflation dynamics.

To address this, in addition to two-way fixed effects (TWFE) models, we incorporated Dynamic Common Correlated Effects (DCCE) estimators. These allow for heterogeneous slopes across departments and explicitly control for unobserved common factors through cross-sectional averages and their lags. Even under this more demanding framework, the central result remains: the average sensitivity of inflation to regional slack is small and statistically weak.

2. Is Composition Driving the Result?

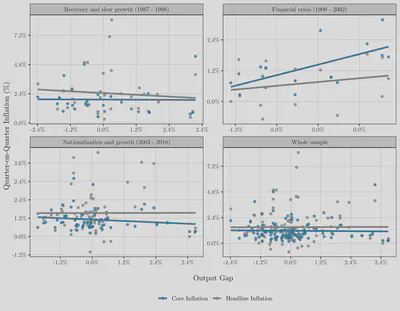

Another plausible explanation is compositional. In small open economies, a significant share of the CPI basket consists of tradable goods whose prices are determined nationally or internationally. If those prices move similarly across departments, they may mechanically dilute any relationship between regional inflation and local activity.

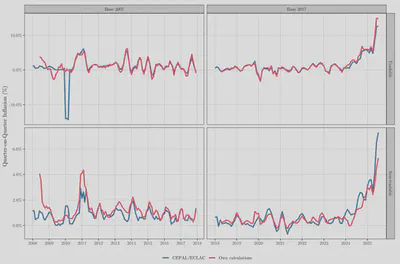

To explore this, we reconstructed departmental series of tradable and non-tradable inflation using INE microdata for the 2007 and 2017 CPI bases. This involved classifying products by tradability, aggregating varieties, linking baskets across bases, and seasonally adjusting the resulting series. We validated the classification by comparing the reconstructed national decomposition with that published by CEPAL. The result is consistent: even non-tradable inflation—the component theoretically most sensitive to local conditions—does not display a robust relationship with the departmental output gap.

3. Uncertainty in Output Gap Measurement

Finally, we addressed measurement uncertainty. The output gap is not directly observable and, in this case, depends on estimated quarterly departmental GDP. Measurement noise could bias the slope toward zero.

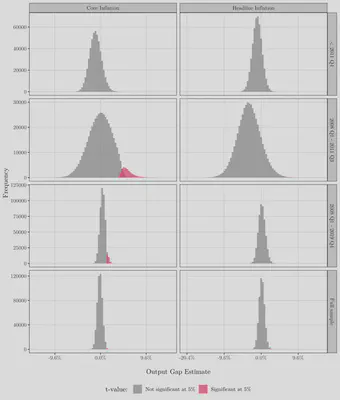

To assess this, we conducted a large-scale simulation exercise: we generated 500,000 alternative output gap series within a plausible range of variation and re-estimated the baseline model for each draw. The distribution of estimated coefficients remains centered around zero. This suggests that the main result does not hinge on a particular output gap measure, but is robust to reasonable perturbations in its construction.

Interpretation: If Not the Cycle, What?

The evidence suggests that inflation dynamics in Bolivia exhibit a strong common component and considerable inertia, while the contribution of regional output fluctuations appears empirically limited.

This finding is consistent with several possible interpretations. Although the paper does not identify a single structural mechanism, the result may reflect a combination of factors:

- The presence of strong common shocks—such as external disturbances, exchange rate movements, or the monetary regime—that affect all regions simultaneously.

- The importance of tradables in the CPI basket, reducing idiosyncratic regional variation.

- Real or institutional rigidities that dampen the transmission from activity to wages and prices, such as labor market informality.

- Sample limitations and inherent measurement challenges in emerging economies.

Rather than isolating a specific cause, the paper documents a robust empirical fact: even exploiting regional variation, controlling for common factors, and allowing for heterogeneity, the estimated Phillips Curve slope remains small.

The normative question then arises: if the central bank cannot significantly influence inflation through the traditional channel of tightening or loosening aggregate demand, how does it do so?

The Current Debate: Expectations and Credibility

If the Phillips Curve appears flat in Bolivia—that is, if inflation responds weakly to the output gap—the relevant question is not whether the mechanism “exists,” but through which channels monetary policy operates.

This issue is particularly salient in the current context, where inflation has reached levels not seen in decades and the Central Bank of Bolivia faces limited room for maneuver.

The paper’s evidence points to two stylized facts: inflation displays a strong common component, and its sensitivity to the cycle is limited. This suggests that expectations and common shocks play a central role. In other words, monetary policy influences inflation primarily through the anchoring of expectations.

Anchoring expectations, however, is not automatic. It requires a credible institutional framework, including:

- Effective central bank independence, not only de jure but de facto, shielding monetary policy from short-term political pressures and fiscal financing needs.

- Credible fiscal frameworks, avoiding fiscal dominance and excessive reliance on monetary financing.

- Clear and consistent communication, helping coordinate expectations around a stable nominal anchor.

In this sense, the challenge for Bolivia’s next government is not only to curb inflation through conventional measures, but to strengthen the institutional framework that allows expectations to remain anchored over time.

Conclusion

In sum, the paper documents a robust empirical finding: the sensitivity of inflation to regional slack in Bolivia is limited, even under demanding specifications and extensive robustness exercises. This does not invalidate the theory, but it does require nuance in how we think about monetary transmission in a small open economy with strong common components.

For readers interested in the full identification strategy, econometric specifications, robustness tests, and detailed discussion of the implications, I invite you to read the complete paper (available here).

For a deeper discussion, see Bordo (2026). ↩︎

See Hazell et al. (2022). ↩︎