Banking in Bolivia as of March 2025: Betting on the Short Term

Introduction

On April 30, ASOBAN published its banking statistics bulletin, highlighting the year-on-year growth of the private banking sector in terms of loans and deposits (5.4% and 5.6%, respectively). It also emphasized the system’s level of provisions (USD 1.634 billion at the official exchange rate) and its strength as reflected in its equity (USD 3.336 billion). Progress was also noted in digital transformation, as measured by the proportion of transfers made via the QR Simple system (91%), and in financial inclusion, reflected in the growth in the number of deposit accounts and borrowers.

While these figures are important and encouraging, it is also essential to consider the system’s challenges in light of the current macroeconomic environment. In this blog post, as usual, we will review some figures from the financial statements of Bolivia’s banking system to provide more context on the current situation and future outlook.

Overview: The Balance Sheet

The balance sheet offers a snapshot of a financial entity’s position at a given moment, reflecting the composition of its assets, liabilities, and equity.

In the case of the banking system, assets represent the resources banks have invested in—such as loans, deposits at other financial institutions, and assets like buildings and equipment. Liabilities are the bank’s obligations, including customer deposits, borrowings from other financial institutions, and other funding sources. Equity is the difference between assets and liabilities, reflecting the bank’s own resources.

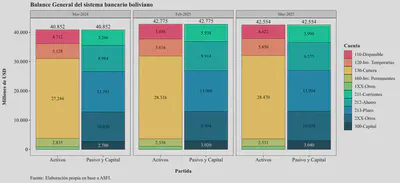

Balance Sheet Composition

The following chart provides a summary of the balance sheet composition of the banking system at three key points: the latest available month, the previous month, and the same month of the previous year. This allows for an analysis of how the financial structure has evolved over the past year and the most recent month:

Compared to March 2024, the balance sheet expanded significantly—by nearly USD 1.702 billion, equivalent to 4.1%. However, compared to the previous month, there was a decline of USD 221 million, mainly due to a sharp drop in cash and equivalents, mirrored by a similar drop in savings deposits. We will explore this further below.

Here is a summary table of the growth:

| Category | Account | 12-Month Change (%) | Monthly Change (%) |

|---|---|---|---|

| Assets | 110-Cash & Equiv. | -1.9% | -8.2% |

| Assets | 120-Temp. Inv. | 14.1% | 0.6% |

| Assets | 130-Loans | 4.5% | 0.5% |

| Assets | 160-Perm. Inv. | -10.7% | -0.3% |

| Assets | 1XX-Others | 15.8% | 1.3% |

| Liabilities | 211-Checking | 13.9% | 1.0% |

| Liabilities | 212-Savings | 6.6% | -3.4% |

| Liabilities | 213-Time Deposits | 0.8% | 0.0% |

| Liabilities | 2XX-Others | 0.1% | 0.4% |

| Equity | 300-Capital | 9.3% | 0.6% |

Overall, we see a reallocation of liquidity from cash to temporary investments, likely due to higher returns on the latter. However, the sharp drop in cash from the previous month is notable. Additionally, checking accounts have grown significantly, while savings deposits have fallen, explaining the drop in liquidity. Equity has also increased.

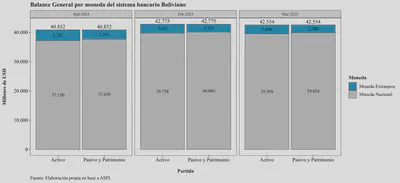

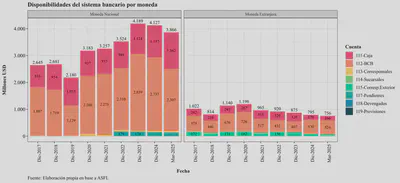

Currency Composition

Another useful way to examine the balance sheet is by separating the share of assets and liabilities in local versus foreign currency:

The chart above highlights Bolivia’s process of “de-dollarization.” Over the past year, banks have returned USD 513 million in foreign currency. Although, on paper, banks are in a “long position”—with more foreign-currency-denominated assets than liabilities—access to those assets is limited. This is because a significant share has been deposited with the Central Bank of Bolivia (BCB), either as legal reserve requirements (classified as cash and equivalents) or to constitute various funds (e.g., CPVIS, FIUSEER) used as collateral for liquidity loans in local currency.

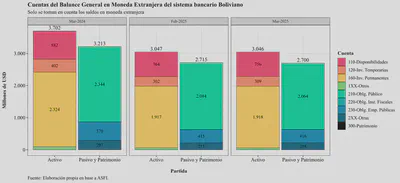

This is further illustrated in the following chart, which shows only foreign currency balances:

Most foreign currency liabilities are public obligations (savings and checking accounts). In contrast, foreign currency assets are classified as permanent investments and cash equivalents. These permanent investments are largely U.S. dollars placed with the BCB. Although they’ve decreased somewhat, they still represent a significant portion of foreign currency assets. In other words, although banks technically own these dollars, they cannot access them because the BCB has not returned the funds.

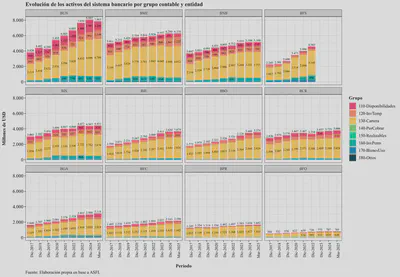

Assets

Bank assets include cash held in vaults and ATMs for daily operations, loans issued (loan portfolio), investments in financial instruments, and real estate used for operations. The loan portfolio remains the most important component, as it is the main source of income for financial institutions. Proper origination and management of the loan portfolio are key to system stability and profitability.

In the current context—marked by economic slowdown and declining Net International Reserves (NIR)—financial institutions have increased their holdings of cash and short-term investments. This reflects a need for liquidity to withstand potential unexpected withdrawals. Accordingly, liquidity management has become a top priority requiring constant monitoring.

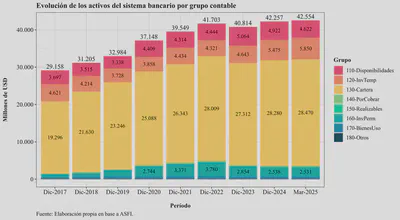

The following chart shows the evolution of banking system assets over the years up to the latest available month. It reveals significant growth with some fluctuations. A key point, as mentioned previously, is the increased preference for temporary investments over cash:

By institution:

The previous chart shows a notable drop in Banco Unión’s assets compared to December 2024.

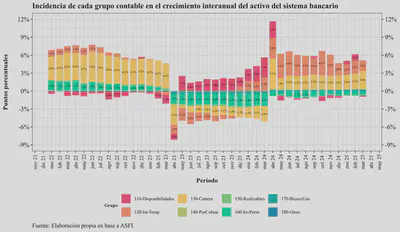

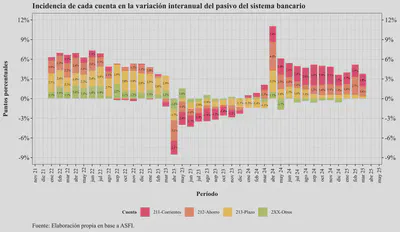

Contribution to Asset Growth

Another approach to analyzing assets is through the contribution of each account group to year-on-year growth. This highlights which groups are driving asset growth and which are offsetting it. The next chart shows the contribution of each group since January 2022:

Here’s how to read it: Between March 2025 and March 2024, total banking assets grew by 4.2%. As the March 2025 bar shows, 3% of this came from loan portfolio growth, 1.8% from temporary investments, and 0.4% from other groups. Offsetting this, permanent investments declined (-0.7%) and cash (-0.2%), summing to the net 4.2% growth.

What does this tell us? Before March 2023, credit growth was the main driver of asset expansion, even prioritized over liquidity. Temporary investments also grew to a lesser extent. However, since March 2023, this trend reversed. Credit and permanent investments began shrinking, while cash and later temporary investments became the focus. This reflects the materialization of macroeconomic risks in Bolivia, notably the unsustainability of the exchange rate due to the drastic fall in BCB reserves, leading to Banco Fassil’s collapse.

Interestingly, as crisis symptoms intensified, banks shifted focus to short-term, low-risk investments. Credit is still growing, but at a slower pace. Given the macroeconomic context, banks are increasingly prioritizing short-term returns—especially as the BCB has tried to absorb system liquidity by offering higher-yield instruments.

Cash & Equivalents

As stated in the Financial Entities Account Manual, cash and equivalents are defined as:

Cash held by the entity in vaults, demand balances at the Central Bank of Bolivia, at the head office and foreign branches, and at domestic and foreign correspondent banks, as well as holdings of precious metals. Also includes checks, other immediately collectible instruments, and pending electronic payment orders.

It is important to note that the BCB’s legal reserve requirements apply to financial institutions’ liquid assets. Thus, institutions must maintain a proportion of deposits in BCB accounts, effectively mandating a minimum level of liquid assets based on deposit volumes.

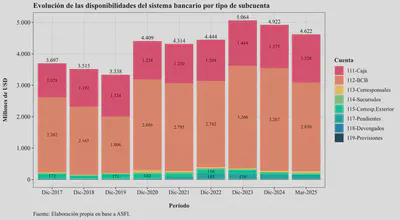

Composition

The following chart shows that system-wide cash and equivalents have remained relatively stable around USD 4 billion. About 30% of this is held in cash for daily operations (withdrawals, ATMs, etc.). However, there was a USD 300 million drop since December 2024, mainly due to decreased BCB balances:

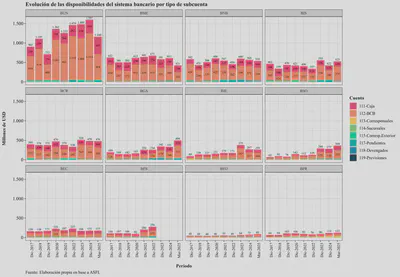

By institution:

By Currency

Due to the aforementioned drop in international reserves and resulting shortage of foreign currency in the economy (cf. this article), foreign currency cash holdings are expected to have declined. This is visible in the following chart:

Temporary Investments

According to the ASFI Financial Entities Account Manual, temporary investments are:

Investments in deposits at other financial intermediation entities, deposits at the Central Bank of Bolivia, and debt securities acquired by the entity, made with the intention of obtaining adequate returns on temporary liquidity surpluses, and convertible into cash within no more than thirty (30) days.

Let’s take a closer look.

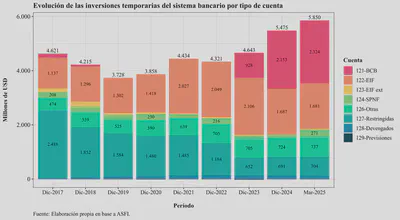

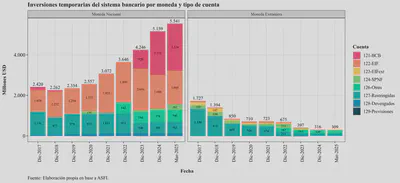

Composition

The next chart shows the composition of temporary investments at year-end and the most recent month. As previously mentioned, exposure to BCB investments has risen significantly since December 2023:

Temporary investments have averaged around USD 4.2 billion in recent years, but have risen sharply in 2024. This year has seen greater concentration in BCB instruments. These include fixed-term deposits, notes, bonds, and other debt securities. As mentioned earlier, the BCB appears to be offering attractive short-term yields, prompting banks to prefer these over traditional loans.

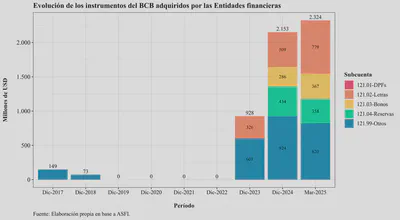

The next image highlights which specific temporary investment types have increased in 2024:

It’s evident that the BCB has used various tools to absorb system liquidity. Of note are instruments labeled as “Complementary Reserves” and “Others,” which lack clear classification, making it difficult to assess their characteristics or risks. This opacity could contribute to financial disintermediation, as banks may prefer BCB securities over lending to the real economy.

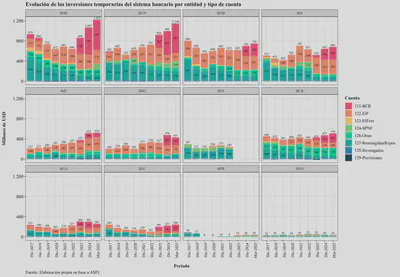

By institution, it’s clear this is not an isolated strategy. The entire financial system has acquired these instruments. The following chart shows temporary investments by entity and sub-account type:

By Currency

It’s also useful to analyze temporary investments by currency. The following chart breaks this down:

Over time, temporary investments have increasingly been concentrated in local currency and BCB instruments. This reflects BCB monetary policy, which, by financing the fiscal deficit, has absorbed system liquidity through debt issuance.

Loan Portfolio

In this section, we analyze the behavior of the Bolivian banking system’s loan portfolio. It is worth noting that the loan portfolio is the main source of financial income and undoubtedly the principal asset of Bolivian banks.

Growth

A key question is how the loan portfolio has grown in recent years. This is important because both rapid and slow growth may signal underlying issues. Rapid expansion could indicate unsustainable credit growth, potentially leading to solvency problems. Conversely, slow growth may point to weak aggregate demand and broader economic challenges.

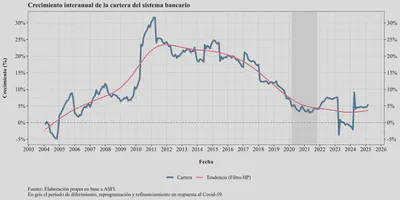

The following chart shows year-on-year growth (current month versus the same month the previous year) of the loan portfolio, excluding provisions and accrued interest. Growth has slowed, stabilizing around 5% in 2024—slightly above levels observed during the pandemic:

The portfolio grew strongly in the second half of the 2010s, peaking around March 2011. Since then, although it remained in double digits, growth decelerated over time.

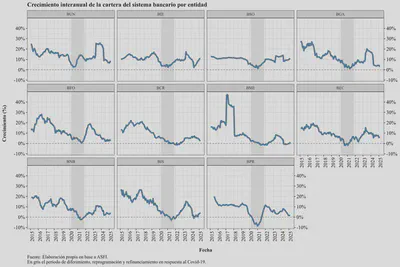

While this suggests a slowdown in credit issuance, it does not necessarily mean individual banks are lending less. With Banco Fassil’s exit in early 2023, the growth base includes a bank no longer in the system. However, as shown below, not all banks have slowed credit issuance:

This chart shows that most banks have experienced significant slowdowns, some even growing more slowly than during the pandemic. This situation warrants close monitoring as it reflects weakening national economic activity and reduced credit demand.

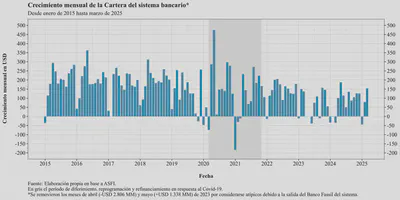

The next chart shows the loan portfolio’s monthly change in dollar terms:

The data reveal that monthly credit flows have been declining, even though balances are still expressed in USD at the official exchange rate.

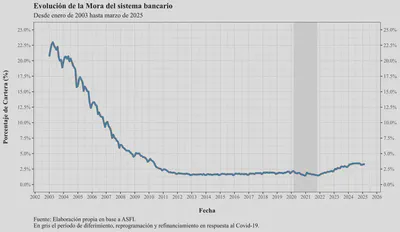

Delinquency

The delinquency ratio (or simply delinquency) represents all loan operations overdue by more than 30 days as a proportion of the total loan portfolio.

The chart below shows the evolution of delinquency since January 2003. In 2003, the ratio reached a critical level—about 23%—which would typically render a banking system insolvent. That period coincided with a particularly difficult economic crisis in Bolivia.

Afterward, delinquency fell under control. By 2007, it was back to single digits, and in 2013 it reached a low of 1.55%. It then began rising moderately to around 1.8% until the pandemic, when loan refinancing and payment holidays temporarily reduced it on paper:

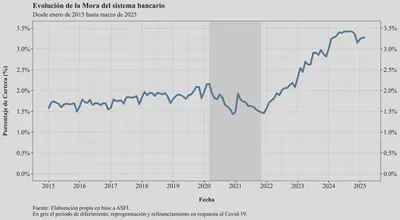

Since the pandemic, the delinquency ratio has resumed its upward trend, posing challenges for financial institutions and regulators. Focusing on data from 2015 onward:

If this situation goes unchecked, it could compromise financial system solvency. In a context of macroeconomic uncertainty, even perceived solvency risk in one or more institutions could trigger a bank run. Crucially, actual insolvency is not required—only the belief that it exists. Thus, financial authorities must closely monitor this indicator and act proactively.

Even though the ratio stabilized or fell slightly in late 2024, macroeconomic problems—such as diesel shortages, dollar scarcity (and a widening parallel exchange rate), and wildfires—could still lead to higher delinquency.

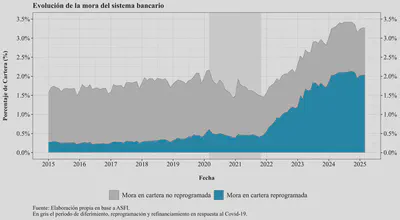

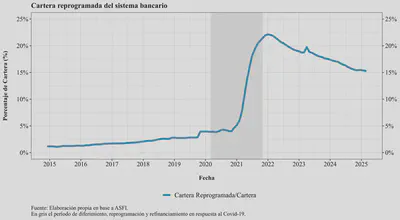

Finally, distinguishing between delinquency in reprogrammed loans versus non-reprogrammed ones, we see that the bulk stems from the former. That is, reprogrammed loans are more problematic:

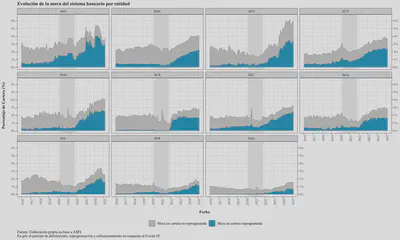

By institution:

Reprogrammed Loans

Reprogrammed loans—more prone to default—still account for about 15% of the total portfolio. While some banks have reduced this exposure, others continue reprogramming. As I noted in a previous blog post:

“In past years, loans were reprogrammed when the borrower could not meet obligations due to (often temporary) reasons. Banks would adjust the payment plan—cutting rates, extending terms, or lowering payments—to avoid loan deterioration. However, if a client cannot pay today, it’s riskier to assume they’ll pay later.”

Reprogrammed loan volumes have declined in recent months as some have matured and overall loan balances continued rising:

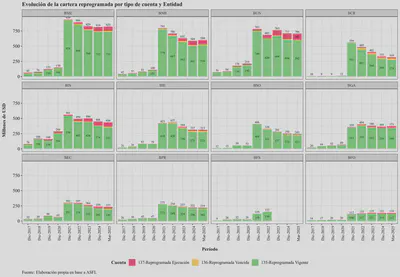

The key issue with reprogrammed loans is their elevated default risk—they have already shown signs of payment difficulties. Monitoring the entire reprogrammed portfolio is essential, not just those currently in default. The chart below shows the reprogrammed portfolio in USD, disaggregated by loan status:

Permanent Investments

According to the Chart of Accounts Manual for Financial Institutions, permanent investments:

Include deposits in financial intermediation institutions, deposits with the Central Bank of Bolivia, debt securities acquired by the institution, and debt certificates issued by the public sector that are not traded on the stock exchange. These investments are not easily convertible to cash, or even if they are, the institution’s investment policy signals an intention to hold them for more than 30 days.

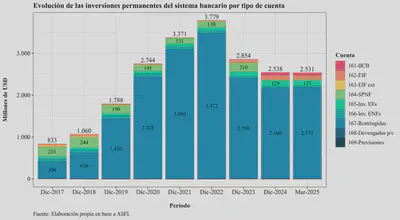

Composition

The following chart shows the composition of these investments by account type:

Most of these investments are concentrated in account 167, which records restricted-availability investments—defined as:

“Investments in securities issued by domestic or foreign entities […] whose availability is restricted, either because of repurchase agreements, additional reserve requirements, or collateral for obligations.”

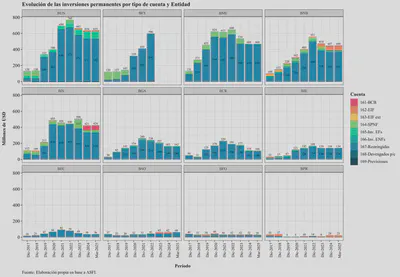

By institution:

…

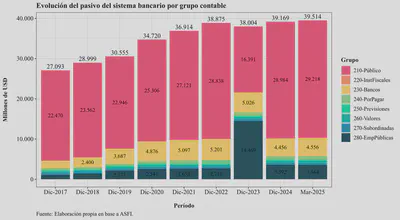

Liabilities

Liabilities are a vital source of funding for financial institutions and essential to their operations. They represent the obligations (debt) that banks owe to the public (deposits), businesses (current accounts), and institutional investors.

In recent months, speculation has grown around banks’ ability to return funds to the public, leading some customers to withdraw deposits. This has posed challenges for banks, which have had to quickly find resources to meet these withdrawals.

The chart below shows the evolution of the banking system’s liabilities at each December since 2015 and includes the most recent quarter available:

From December 2023, we see an increase in account 280, reserved for public enterprises. This stems from the accounting reclassification of pension funds, now managed by the state-run Gestora Pública instead of private pension fund administrators (AFPs). Nearly 40% of banking sector funding is now concentrated in a single entity, raising concerns over liquidity management due to the significant market power this concentration represents. This reclassification was reversed mid-2024, as seen in the June 2024 figures.

Overall, liabilities have grown modestly during the year—about USD 93 million per month. If banks cannot attract public deposits, they cannot sustain loan issuance, which is their main business. The available options are to raise interest rates to attract deposits or negotiate directly with Gestora Pública for funding—also at higher rates. However, because interest rates on social housing and productive credit are fixed, raising deposit rates reduces bank profitability.

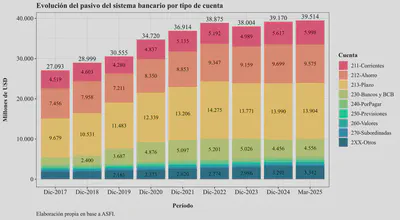

Alternatively, liabilities can be broken down by deposit type:

The chart shows that savings accounts and time deposits have slightly declined since December last year, while current accounts have increased, offsetting the fall in the other categories.

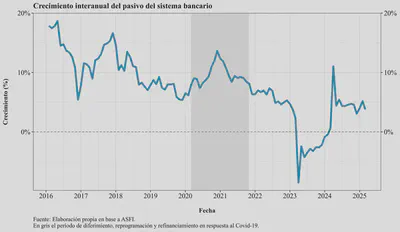

Growth

How has the banking system’s liabilities evolved? Overall, liabilities have continued growing year-over-year, but at a decreasing rate:

This chart should be interpreted with caution. As in the case of loans, the base for year-over-year comparison includes Banco Fassil, which was still operational a year ago. The current system has yet to fully recover the deposit levels from before that liquidation.

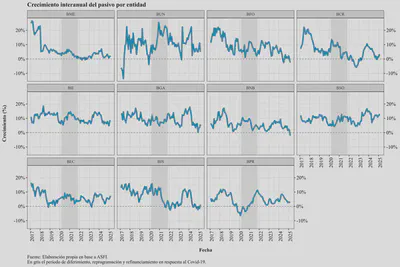

Looking at year-over-year growth by institution:

The chart shows that banks are generally having difficulty attracting funds. While most are still growing year-over-year, their growth is slower than in previous years.

Contribution to Growth

As with asset growth, liability growth can be broken down by type of account. The following chart shows this disaggregation—essentially the mirror image of the asset side:

What can we infer? Before March 2023, time deposits led liability growth, followed by savings accounts. Although more expensive, these are more stable and help banks match loan maturities. Since March 2023, however, current account growth turned negative. By year-end, even time deposits showed negative growth. From April 2024, liabilities began growing again, led by current accounts and, secondarily, savings accounts. While this shift is not inherently problematic, it does expose banks to greater liquidity risk, as current and savings accounts are more volatile and more likely to be withdrawn in times of uncertainty—as was seen in 2023.

Income Statement

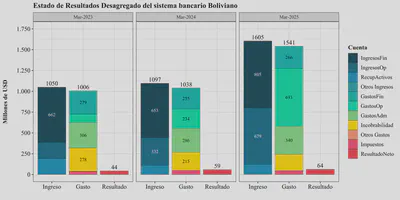

Finally, although we won’t go into detail, below are the financial results for the Bolivian banking system as of September for the past three years:

For example, we see that the scale of the business has grown in recent years. As of March 2025, the banking system posted a net result that was comparatively better than in the same month in previous years. However, these results should be interpreted with caution, as they must be adjusted for inflation and exchange rate effects and evaluated relative to the capital (and risk) taken on.

With that said, we observe a slight shift in income sources from financial revenues (from loans) to operational revenues (from commissions), mirrored by corresponding changes in costs. In fact, while both operational revenues and expenses have grown, expenses have done so at a faster pace.

Conclusion

1. Increased focus on short-term banking activity: The composition of banking assets reveals a growing preference for short-term instruments, especially temporary investments. These have gained importance relative to the loan portfolio, signaling a strategic shift by financial institutions toward more liquid and less risky assets. This behavior is driven by the challenging macroeconomic environment, where risk and liquidity expectations are highly sensitive.

2. Growing preference for the Central Bank of Bolivia as counterparty: Data show a strong channeling of liquidity surpluses toward the BCB, through both cash and temporary or permanent investments. Banks have concentrated their liquidity in BCB-issued instruments—including those recorded as “complementary reserves” or “other”—which are not always fully transparent. This implies higher institutional exposure to a single counterparty and less risk diversification in bank portfolios.

3. Slowing credit growth and rising risk in reprogrammed loans: Credit growth has steadily moderated to around 5% and shows increasing vulnerability, evidenced by the rising delinquency rate, particularly among reprogrammed loans. These loans account for a significant portion of the total (about 15%) and continue to pose repayment challenges. If not properly managed, this represents a latent risk to financial stability.

4. More volatile bank funding and higher vulnerability to confidence shocks: On the liabilities side, while overall funding has continued to grow year-over-year, it has increasingly shifted toward current and savings accounts, and away from time deposits. This exposes institutions to greater liquidity risk, as these sources are more susceptible to withdrawal during uncertainty.

5. Financial disintermediation: The combination of slower loan growth, increased BCB exposure, and greater internal investment in financial instruments may be driving a form of financial disintermediation. In other words, banks may be shifting away from their traditional role of channeling savings into productive investment and increasingly acting more like institutional investors than lenders to the real economy.