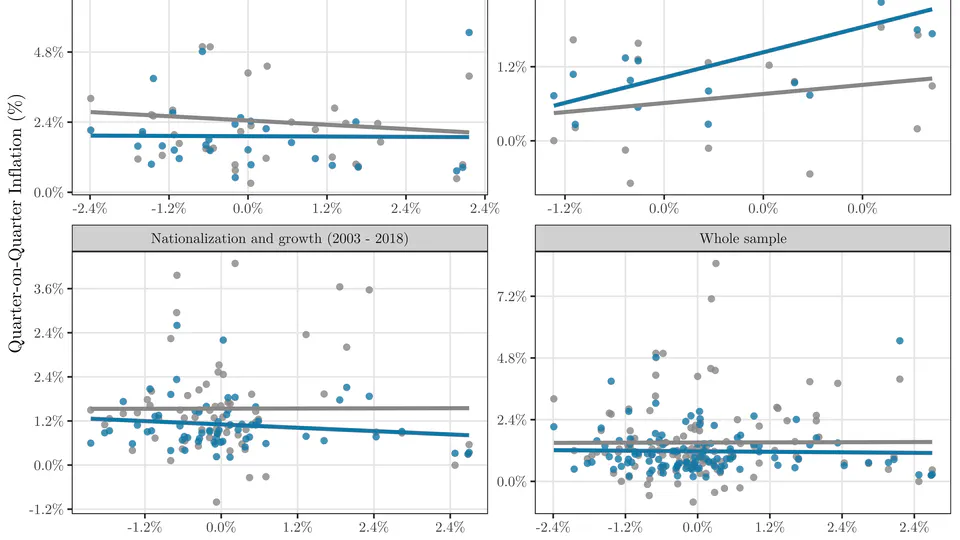

This paper estimates the relationship between inflation and the output gap at the departmental level in Bolivia, using quarterly data for the period 1993–2019. Despite substantial subnational variation, the association between inflation and economic slack is small and statistically indistinguishable from zero. This result holds across multiple specifications, including estimators that control for common factors and allow for regional heterogeneity. Even when separating tradable and non-tradable inflation, the relationship remains weak. The evidence suggests that inflation dynamics in Bolivia exhibit a strong common component and limited sensitivity to regional cyclical conditions, with important implications for understanding monetary policy transmission in a context of elevated inflation and institutional constraints.

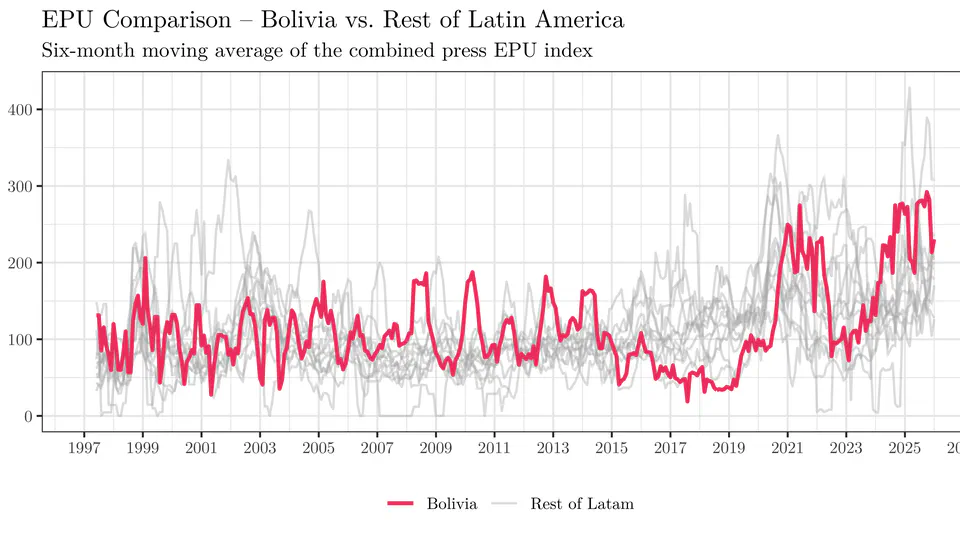

In this post I analyze the Economic Policy Uncertainty (EPU) Index recently published for Bolivia and other Latin American countries by the Bank of Spain. Using these data, I explore the recent evolution of economic uncertainty in Bolivia, its comparison with the rest of the region, and its possible relationship with recent political events. The results suggest that Bolivia remains among the countries with relatively high levels of uncertainty, reinforcing the importance of predictable economic policies and institutional frameworks based on clear rules. Reducing discretion in public policy can help strengthen economic confidence and create more favorable conditions for investment and growth.

As demand for reproducible macroeconomic analysis grows, manually extracting data from international organizations becomes a bottleneck: processes are poorly documented, non-scalable, and difficult to automate. SDMX —the statistical standard adopted by the IMF, ECB, OECD, World Bank, and others— offers a structured solution that makes it possible to find, understand, and extract data consistently through APIs. This post provides a practical introduction to how the SDMX model works, how to identify dataflows, structures, and codelists, and how to build reproducible queries in both XML and JSON. Using examples from the IMF (WEO) and the ECB (€STR), it shows a generalizable workflow for automating macroeconomic series in R, culminating with the use of the imfapi package, which abstracts much of the technical complexity.

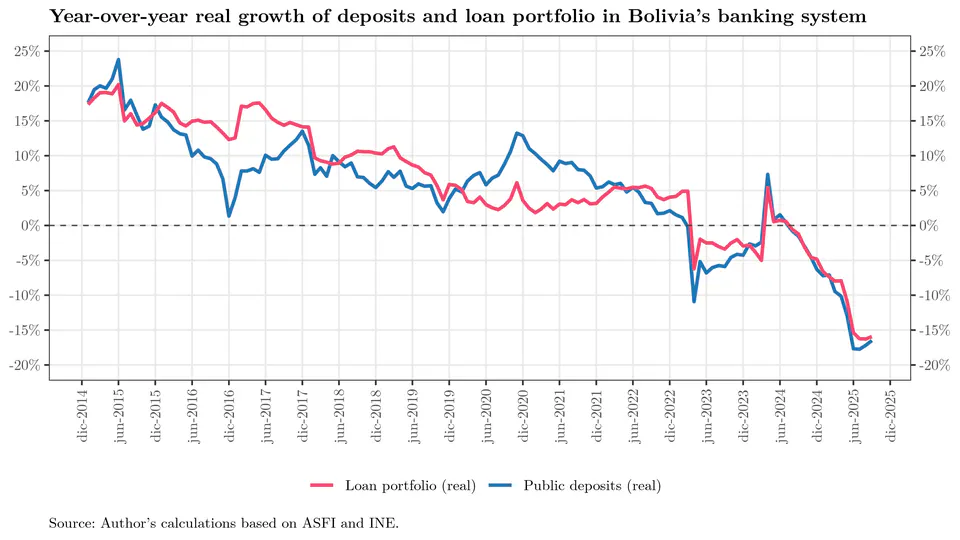

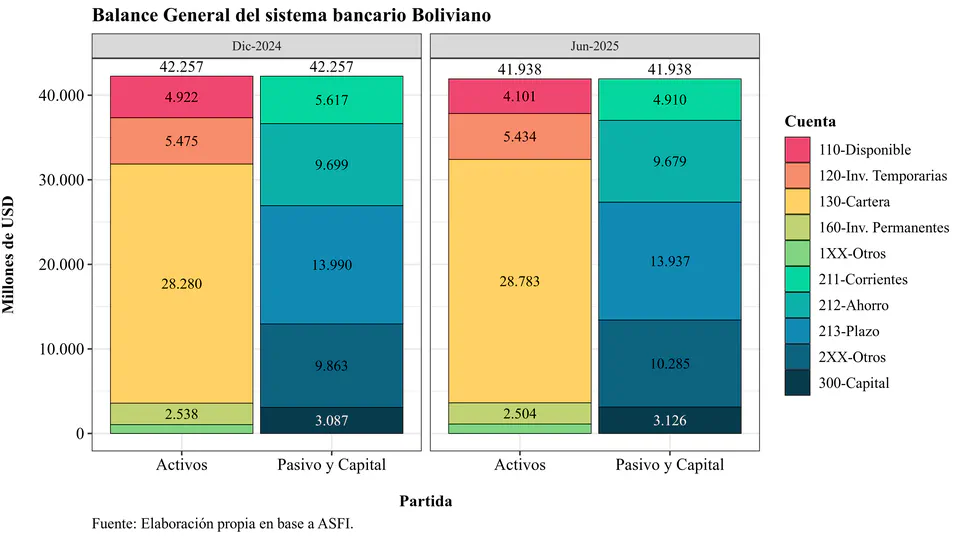

As of September 2025, the Bolivian banking system is operating in a defensive mode amid a fragile macroeconomic environment: the balance sheet expanded by +3.6% in nominal terms (≈ USD 1.479 billion at the official exchange rate), but credit and deposits contracted in real terms. Growth is concentrated in short-term liquid assets —cash and temporary investments— with greater exposure to the BCB and a rebound in account 124 (TGN), while loan portfolio growth has slowed. Funding has become more volatile, with a declining share of time deposits and increased reliance on savings and current accounts, in a context of USD scarcity and a “dual” exchange market. Asset quality remains under strain due to the reprogrammed portfolio (~15%), the main driver of non-performing loans. Despite a positive and recovering ROE, margins are under pressure (regulated lending rates and the need to raise deposit rates), reflecting reduced financial intermediation and growing dependence on the BCB for liquidity management.

This article shows how to extract economic data from the IMF using its DataMapper API, with `R` functions to organize and analyze information on indicators and countries. Applications are illustrated with Bolivia and Spain, demonstrating how to access structured data such as GDP growth, unemployment, inflation, fiscal balance, and public debt.

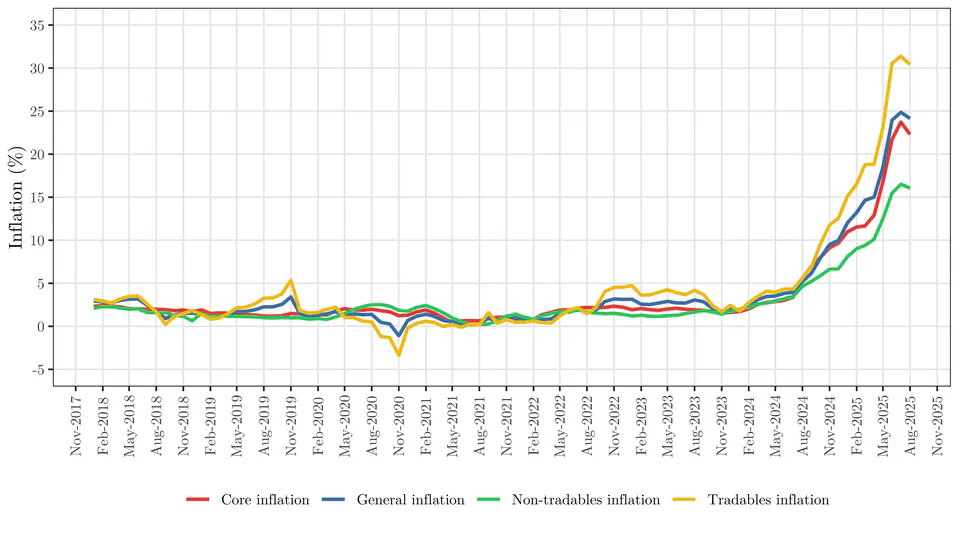

This article explores data extraction from ECLAC and its application to the analysis of inflation in Bolivia, using the R programming language to access relevant economic data. As of August 2025, Bolivia’s year-on-year inflation ranges from 16.05% (non-tradable goods) to 30.43% (tradable goods).

As of June 2025, the Bolivian banking system maintains a defensive strategy in response to a deteriorating macroeconomic environment. Balance sheet expansion is concentrated in temporary investments, mainly in instruments issued by the BCB and now also by the TGN, to the detriment of credit, whose growth is slowing and showing higher risk, especially in reprogrammed loans. Bank funding is becoming more volatile, with less reliance on term deposits and increasing dependence on savings and checking accounts. Although profitability is improving, it is doing so through low-risk, highly liquid assets, reflecting reduced financial intermediation and growing dependence on the BCB.

Since late 2023, Bolivia has been experiencing an accelerated and widespread inflationary process, with year-on-year inflation reaching 23.96% in June 2025 and sharp increases in both tradable goods —affected by the dual exchange rate— and non-tradables, as well zas core inflation. The persistent fiscal deficit, financed by the Central Bank through monetary issuance, has weakened the exchange rate regime, eroded institutional credibility, and limited the BCB's ability to control inflation. Without credible fiscal consolidation and the restoration of the Central Bank's autonomy, inflationary pressures will continue to intensify.

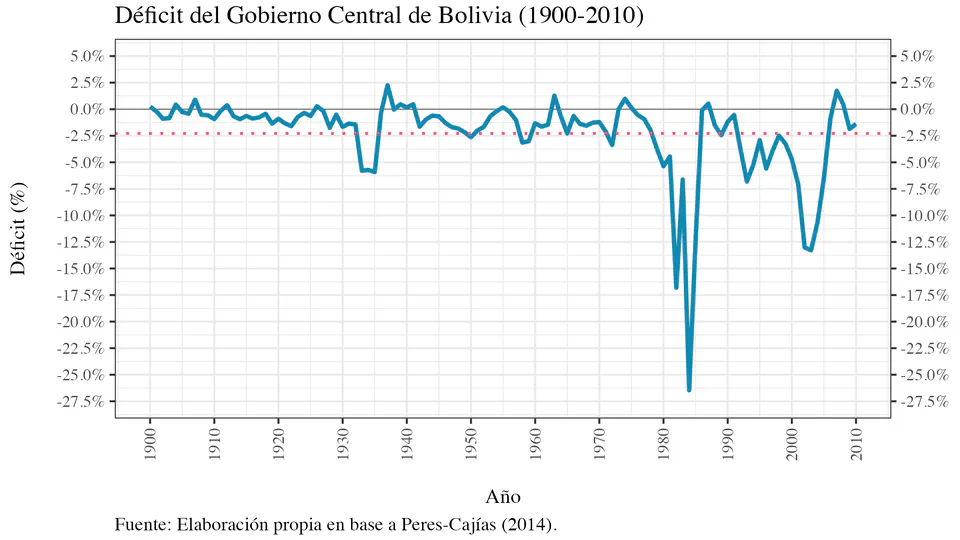

In recent years, Bolivia has experienced a persistent inability to maintain fiscal balance, exacerbated by its dependence on extraordinary revenues from natural resources. Moreover, in recent months, inflation has accelerated, surpassing double digits. This post analyzes, from a historical perspective, how recurring fiscal deficits and their financing through the Central Bank have contributed to inflationary cycles. Based on this diagnosis, two concrete proposals are presented—a fiscal rule and the reform of Article 22 of the BCB Law—as complementary measures to strengthen macroeconomic sustainability.

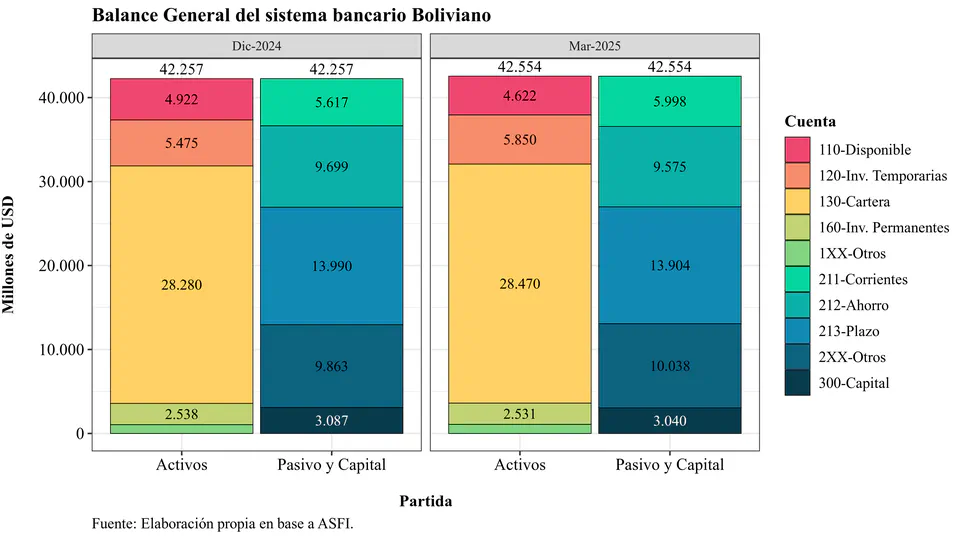

As of March 2025, Bolivia's banking system shows clear signs of a short-term-oriented strategy in response to a challenging macroeconomic environment. Balance sheet expansion has focused on temporary investments, particularly in instruments issued by the Central Bank (BCB), reflecting increased liquidity channeled to that institution. Meanwhile, credit portfolio growth has slowed (5.4% annually), and banks face challenges in attracting time deposits, relying increasingly on current and savings accounts, which are more volatile and sensitive to confidence shocks. Delinquency remains high and is concentrated in rescheduled loans, still representing around 15% of the total. While system profitability has improved, it has done so by leveraging low-risk, highly liquid placements, suggesting reduced financial intermediation to the real economy. Overall, the system is protecting itself, prioritizing liquidity, but sacrificing credit depth in a context of structural fragility and growing dependence on the BCB.